Chapter 18 Financial Procedures

The Committee believes that this [better scrutiny of the estimates] can be achieved by improving the parliamentary processes to consider the estimates, ensuring that parliamentarians have clear and understandable estimates information, and providing sufficient support and capacity for Members to interpret the information available.

STANDING COMMITTEE ON GOVERNMENT OPERATIONS AND ESTIMATES, Seventh Report

“Strengthening Parliamentary Scrutiny of Estimates and Supply”, presented to the House on June 20, 2012 (Journals, p. 1876)

The development of parliamentary procedure is closely bound up with the evolution of the financial relationship between Parliament and the Crown. As the executive power,1 the Crown is responsible for managing all the revenue of the state, including all payments for the public service.2 The Crown, on the advice of its Ministers, makes the financial requirements of the government known to the House of Commons which, in return, authorizes the necessary “aids” (taxes) and “supplies” (grants of money). No tax may be imposed, or money spent, without the consent of Parliament.

The direct control of national finance has been referred to as the “great task of modern parliamentary government”.3 That control is exercised at two levels. First, Parliament must assent to all legislative measures which implement public policy and the House of Commons authorizes both the amounts and objects or destination of all public expenditures. Second, through its review of the annual departmental performance reports, the Public Accounts and the reports of the Auditor General, the House ascertains that no expenditure was made other than those it had authorized.4

The practices and procedures which govern how Parliament deals with the nation’s finances are set out principally in the Constitution Act, 1867,5 the Financial Administration Act,6 unwritten conventions, and the rules of the House of Commons and the Senate.

Basic Components of Financial Operations

The basic components of parliamentary financial procedure may be succinctly described as follows:

Consolidated Revenue Fund: the account into which the government deposits taxes, tariffs, excises and other revenues, once collected, and from which it withdraws the money it requires to cover its expenditures.7

Royal Recommendation: the message from the Governor General required for any vote, resolution, address or bill for the appropriation of public revenue.8 Only a Minister can obtain such a recommendation.

Supply: the process by which the government submits its projected annual expenditures (the estimates) for parliamentary approval.

Borrowing authority: the authorization required by the government to make up any shortfall between revenues and expenditures.

Ways and means: the process by which the government sets out its economic policy (the budget) and obtains the necessary resources to meet its expenses.

Public Accounts: the annual statement and review of the government’s financial transactions.

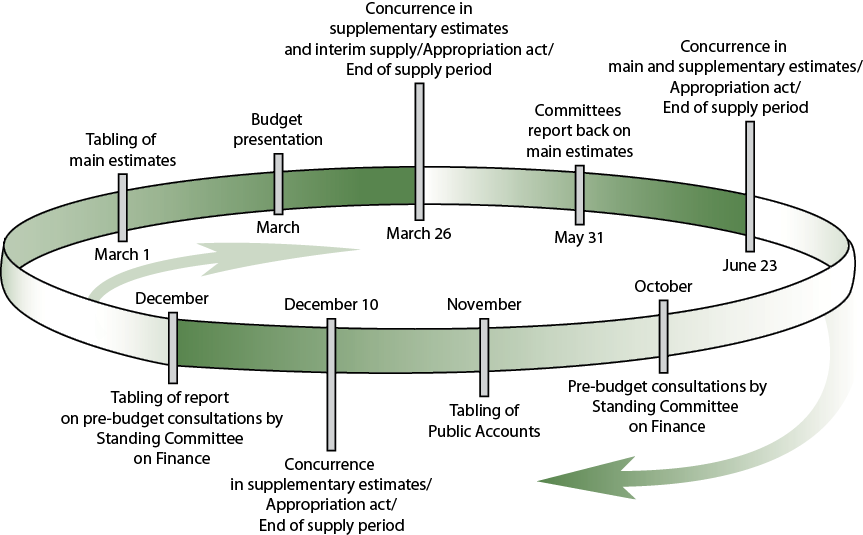

The Financial Cycle

The fiscal year of the Government of Canada runs from April 1 to March 31.9 However, the planning for the fiscal year begins much earlier with the preparation of departmental expenditure plans, which are developed in accordance with the government’s policy and budgetary priorities, and the pre-budget consultations by the Standing Committee on Finance.10 The expenditure plans are submitted to the House in their consolidated form as the main estimates. At the same time, the Department of Finance is compiling the information taken in during the pre-budget consultations and preparing its economic forecasts. The government’s efforts to reconcile its spending obligations and revenue projections are reflected in the budget.

The budget outlines the government’s fiscal, social and economic policies and priorities, while the estimates set out in detail its projected expenditures for the upcoming fiscal year. Usually, the budget is presented in February or March, although the government is under no obligation to do so, or even to present an annual budget at all.11 Under normal circumstances, the main estimates are tabled in the House on or before March 1 and submitted for concurrence by the House no later than June 23.12

Should the government require funds while waiting for, or in the absence of, income from taxes and other revenue sources, it may borrow funds. Should there be a change in the government’s requirements as set out in the main estimates, Parliament will be asked to approve one or more supplementary estimates.

The tabling of the Public Accounts of Canada and the Annual Report of the Auditor General, and their review by the Standing Committee on Public Accounts, completes the government’s annual cycle of financial transactions.13

Historical Perspective

The manner in which Canada deals with public finance derives from British parliamentary procedure as practised at the time of Confederation.14 The financial procedures adopted by the Canadian House of Commons in 1867 were formed by the following principles:

- that although Parliament alone might impose taxes and authorize the use of public money, funds can be appropriated to Parliament only on the recommendation of the Crown (royal recommendation), in Canada represented by the Governor General;

- that the House of Commons has the right to have its grievances addressed before it considers and approves the financial requirements of the Crown;

- that the House of Commons has exclusive control over the business of public finance (taxing and spending) and all such business is to be initiated in the lower House;15 and

- that all legislation sanctioning expenditure or initiating taxation is to be given the fullest possible discussion, both in the House and in committee.16

British Precedents

The whole law of finance, and consequently the whole British constitution, is grounded upon one fundamental principle, laid down at the very outset of English parliamentary history and secured by three hundred years of mingled conflict with the Crown and peaceful growth. All taxes and public burdens imposed upon the nation for purposes of state, whatsoever their nature, must be granted by the representatives of the citizens and taxpayers, i.e., by Parliament.17

The requirement that legislation sanction all public spending and taxation has a long constitutional history.18 In medieval England, the King was expected to meet most public expenses (the court, the clergy and the military) out of his personal revenues. Where this was not possible, he was obliged to seek funds by summoning the common council of the realm, or Parliament, to discuss what aids (taxes and tariffs) should be supplied to support the Crown. Even in the earliest days of these assemblies, it was generally recognized that when aids or supplies were required, the King should seek consent not only to impose a tax, but also for the manner in which the revenues from that tax might be spent. In 1295, the writ of summons for one of these councils, later known as the Model Parliament, proclaimed: “What touches all should be approved by all”.

Early English Parliaments were not legislative bodies as we understand them today, but petitioning bodies. They presented petitions to the King and agreed to taxes (i.e., money granted to the Crown), on the condition that certain problems or grievances outlined in the petitions would be addressed or concessions made. By 1400, the Commons insisted that the King respond to their petitions before any grant of money was made. When the King refused, they adopted the practice of delaying the grant until the last day of the session.

The councils subsequently divided into two Houses based on their communities of interest: the House of Lords and the House of Commons. In principle, each House taxed itself independently; for this reason it was not considered appropriate that the Lords determine what the Commons should contribute. Moreover, because the greater part of the tax burden fell to the Commoners, grants to the Monarch came to be made “by the Commons with the advice and consent of the Lords”. The dominant position of the Commons in terms of deciding matters of taxation was firmly established early in the 15th century when Henry IV conceded that any grant to the Sovereign must be agreed upon by both the Lords and the Commons and must be communicated to the Crown by the Speaker of the House of Commons.19

Initially, the Commons were content simply to have grants of supply originate in their House. However, over time the Lords began tacking on additional legislative provisions to Commons “money bills”, by way of amendments. This was viewed by the House as a breach of its prerogative to originate all legislation which imposed a charge either on the public or the public purse, and led the Commons, in 1678, to resolve that:

All aids and supplies, and aids to his Majesty in Parliament, are the sole gift of the Commons; and all Bills for the granting of any such aids and supplies ought to begin with the Commons: and that it is the undoubted and sole right of the Commons to direct, limit, and appoint, in such Bills, the ends, purposes, considerations, conditions, limitations, and qualifications of such grants; which ought not to be changed or altered by the House of Lords.20

By the end of the 17th century, the principles of modern financial procedure, most particularly the annual treatment of finance by the House of Commons and the notion of effective and permanent House control over all public expenditure, were well established. Their evolution had taken several centuries and was related to the rise and gradual abolition of the Civil List, the creation of the Consolidated Fund and the growth of the estimates system, whereby the government receives annual operating grants from Parliament.

The Civil List

The Civil List21 was initially a list of all non-military personnel in the service of the Crown for whom remuneration was paid for by Parliament.22 These included individuals in the personal employ of the Sovereign, such as domestic servants, people in the diplomatic service and various public officials and civil servants. Previously, the Crown had covered these expenses out of the Sovereign’s hereditary revenues and certain taxes voted to the Sovereign for life by Parliament.

Initially, Parliament did not concern itself with how the funds were spent. In general, it was felt that, while the Crown was not entitled to increase its revenue without Parliament’s consent, it was perfectly free to dispose of, as it pleased, any funds properly in its possession. However, the amounts voted by Parliament were frequently insufficient and the House was increasingly asked for additional grants to discharge debts which the Sovereign had incurred to cover the shortfall. So emerged the practice of allocating to the Crown funds for specific purposes.

With the accession of Queen Victoria to the throne in 1837, Civil List expenditures were reduced to those required solely to meet the personal needs of the Sovereign and her family. All other civil expenses were taken over by the national treasury and paid out of the Consolidated Fund.

The Consolidated Fund

During the 17th and 18th centuries, the raising and spending of public money were intimately connected. Requests from the Crown for money, in estimated amounts for specified purposes, were considered and approved by a Committee of the Whole House. This phase concluded, a second Committee of the Whole considered the recommended ways and means for raising the money required to cover the amounts approved. The work of the first committee, which came to be known as the Committee of Supply, led directly to the work of the second, the Committee of Ways and Means. Only when the latter came to a decision would a bill be introduced which empowered the Crown to raise money in the amount of and in the manner approved by the Committee of Ways and Means and to spend up to the amount approved, and only for the purposes designated, by the Committee of Supply.

The close coupling of taxing and spending continued until 1786 when the establishment of the Consolidated Fund23 abolished the need to match a particular outlay with a specified revenue.24 Once the Committee of Supply had agreed to the expenditure of certain sums, the Committee of Ways and Means would look to the Consolidated Fund to pay for the approved expenditures. The concept of an appropriation bill was introduced to set aside from the Fund the amounts required for the purposes designated. Appropriation bills merely set aside funds; they do not require the Crown to spend all or any of the money which has been appropriated. Furthermore, appropriations are always made with a time limit; the spending authorization provided under an appropriation act expires at the end of the fiscal year to which the act applies.25

Thus, two distinct kinds of government financial business emerged: the business of supply, which approved expenditures and their purposes and resulted in the passing of appropriation bills; and the business of ways and means, which resulted in the taxation bills used to raise the monies needed to replenish the Consolidated Fund.

Since the institution of the Consolidated Fund, all expenses of the state have been authorized either by specific statute (ongoing and permanent) or by way of an annual appropriation. It is the annual appropriations, or supply grants, which come before the House for discussion each year.

The Estimates

As the 17th century drew to a close, England’s continuing colonial disputes with France and Spain and the recent experience of two civil wars made evident the need to maintain a national standing army under the control of Parliament. Previously, the Monarch had simply raised armies to fight wars, as required.

The institution of a permanent military establishment carried with it the requirement for grants to cover the cost of personnel, wars and fortifications.26 In 1689, the English Parliament passed the Mutiny Act, legislation which had to be renewed yearly. The Act restricted the use of martial law and gave authorization for a definite number of military personnel. The Act also authorized a grant of funds sufficient to cover military wages, ordnance and shipbuilding for that year. This, then, was the means by which Parliament undertook the regular annual charge of supply for the army and navy, and from which emerged the parliamentary practice of granting annual appropriations for the operations of government. The principles governing that practice hold that the government may spend on public administration no more than the amounts (estimates) approved by Parliament and is similarly prohibited from using funds voted for one purpose to pay for another (engaging in virement).27 As the scope of civil government expanded, civil expenditure came to comprise a number of expenses funded solely by annual parliamentary grants.28

Financial Procedure in Colonial Canada

By the end of the 18th century, most of the British North American colonies had acquired representative political institutions.29 For many years, colonial governance was fraught with dissension as a result of the often irreconcilable interests of appointed governors and elected representatives. Much of that conflict arose over the issue of who should control the public purse.30 However, by the time of Confederation, the popular assemblies of British North America had asserted their right to decide what taxes should be raised and where they would be spent, thus fulfilling the principle of responsible government, which holds that the executive may govern only while it enjoys the confidence or support of the House of Commons. Parliament’s rights and role in the processes of taxing and spending may be found in the various rules and procedures of the legislatures from which they derive.31 In 1867, the Canadian House of Commons adopted the rules of the former Legislative Assembly of the Province of Canada, including those covering the process of taxing and spending.32

Upper Canada

Initially, the colonial administration of Upper Canada was paid for entirely by the British Parliament. However, in 1817, the Executive asked the Assembly for a grant of money to cover certain administrative costs which exceeded the amount authorized by Westminster. Previously, Britain had covered any excesses but, in view of the growing wealth and relative prosperity of the colony, the local community was asked to subsidize these expenditures. Not surprisingly, the elected representatives demanded a say in how the money would be spent. Moreover, they asked that the Governor and his Executive Council not spend money which the Assembly had not authorized, nor for purposes other than those it had designated.

Supply (the authority to spend) was rarely withheld.33 Even when it was withheld (in 1818, 1825 and 1836), it was inconsequential. In fact, the Crown appeared relatively indifferent to the sums voted by the House. Nonetheless, the House continued to take the supply process seriously, resolving that the misapplication of parliamentary appropriations was a “high crime” and affirming the undoubted right of the elected House to determine how, and how much, public money was spent.

By 1840, supply proceedings in the Assembly had become relatively formalized. Estimates were referred upon presentation to a permanent Select Committee on Finance. The committee’s report would be referred to a Committee of Supply (a Committee of the Whole House)34 which, in turn, would report back to the House a number of resolutions, each recommending that money be appropriated for some item. Once adopted, these resolutions would be referred to a special committee of two members charged with drafting the bills based thereon. A number of bills would then be presented.

Lower Canada

Prior to 1818, the Executive Council requested no funds from the House of Assembly of Lower Canada, with the result that no estimates were tabled. Nevertheless, the House attempted to exert some financial control by way of its annual review of the public accounts. Until 1812, the accounts were examined in a Committee of the Whole, after which they were referred to a special committee of five members. Beginning in 1818, estimates were also referred to this committee. The committee’s frequent criticisms of the administration for appropriating money without the consent of the House of Assembly prompted the House to resolve that the appropriation of the public revenue without legislation was “a breach of the privileges of this House, and subversive of the Government of this Province, as established by Law”. The House further warned that it would hold the Receiver General responsible for all monies levied.35

The House of Assembly used various other procedures in its efforts to control the administration, including refusing supply, refusing to deal with all legislation until basic grievances were met and tacking on clauses to bills appropriating revenue for which there was no existing statute, a practice which forced the executive to choose between enacting the additional clauses or losing supply.

The Province of Canada

In 1840, the British Parliament passed the Union Act uniting Upper and Lower Canada.36 With its enactment came the acknowledgement that a government should enjoy the confidence of the people’s representatives.37 It is also by the Union Act that the royal prerogative in right of financial legislation was first introduced into Canadian parliamentary law. Prior to 1840, any elected member in the legislatures of Canada could introduce a bill with financial implications for consideration of the assembly. This practice was much frowned upon by governors on the grounds that it interfered with the efficient operation of government.38 Lord Durham felt strongly that the “prerogative of the Crown which is constantly exercised in Great Britain for the real protection of the people, ought never to have been waived in the Colonies; and [that if] introduced … it might be wisely employed in protecting the public interests, now frequently sacrificed in that scramble for local appropriations, which chiefly serves to give an undue influence to particular individuals or parties”.39

Provision was made for a Consolidated Revenue Fund against which would be charged all expenses related to the collection, management and receipt of revenue, all interest on the public debt and remuneration of the clergy and officials included on the Civil List.40 Any surplus remaining in the fund after these charges had been deducted could be used for the service of the public, as the legislature thought fit.41 All votes, resolutions or bills involving expenditure of public funds were to be first recommended by the Governor General.42

There were still disputes over the control of money. However, no administration was defeated over an appropriation act; in fact, even when governments changed, a supply bill was often taken over and carried through by the succeeding administration.43 By 1867, the vote of confidence had virtually replaced withholding supply as the preferred mechanism by which the Assembly sought control over the administration of government.

Financial Procedure in the Canadian House of Commons

The Constitution Act, 1867 provided that any bill appropriating any part of the public revenue or imposing a tax or duty must originate in the House of Commons.44 Furthermore, the Act made it unlawful for the House to pass any measure to appropriate any part of the public revenue, or of any tax or duty, which had not first been recommended by the Governor General in the session in which the measure was proposed.45 Additional clauses provided for the creation and use of a Consolidated Revenue Fund by the Parliament of Canada for the public service.46

Standing Orders (1867-1968)

The first Standing Orders of the House of Commons codified long-established rules of parliamentary practice and procedure which were rooted in British parliamentary history and, subsequently, also in the rules and procedures of the different colonial legislatures.

The cardinal principle governing Parliament’s treatment of financial measures was that they be given the fullest possible consideration in committee and in the House. This was to ensure that “parliament may not, by sudden and hasty votes, incur any expenses, or be induced to approve of measures, which may entail heavy and lasting burthens upon the country”.47 To satisfy the requirement for debate, the 1867 rules required that financial business be considered first in a Committee of the Whole before being debated in the House.48 In 1874, the House agreed to appoint, henceforth, at the beginning of each session, a Committee of Supply and a Committee of Ways and Means.49 The Committee of Supply approved the annual estimates of government expenditure, while the Committee of Ways and Means considered the government’s proposals to raise revenue and approved necessary withdrawals from the Consolidated Revenue Fund for the measures in the estimates. Yet another measure safeguarding the House from hasty financial decisions was the rule that the debate on any motion proposed “for any public Aid or Charge upon the people” would not proceed immediately, but would be adjourned to a subsequent sitting day.50 This was done so that “no member may be forced to come to a hasty decision, but that every one may have abundant opportunities afforded him of stating his reasons for supporting or opposing the proposed grant”.51

The first Standing Orders also included, directly under the heading “Aid and Supply”, a note in reference to the Constitution Act, 1867, which required that any measure seeking to raise or spend public money be initiated by the Crown. The rules provided further that all legislation respecting charges upon the public revenue (expenditure) or on the public (taxation) be introduced first in the House of Commons; that is, the Commons alone grants supply.52

In general, the financial procedures set out under these rules remained the same for the next 100 years.53 However, financial procedures came to be used by successive oppositions as a means of obstructing, delaying and even preventing the government from passing financial business. As a consequence, beginning in the late 1960s, financial procedures, which had remained virtually unchanged for a century, were drastically revised and streamlined. These revisions had to recognize and protect two apparently contradictory principles: that the government is entitled to get its financial legislation through Parliament, and that the opposition is entitled to identify, draw attention to, delay and debate items that it feels need attention and discussion.

The Royal Recommendation

Under the Canadian system of government, the Crown alone initiates all public expenditure and Parliament may authorize only spending which has been recommended by the Governor General.54 This prerogative, referred to as the “financial initiative of the Crown”, is the basis essential to the system of responsible government and is signified by way of the “royal recommendation”. With this prerogative, the government is assigned the responsibility for preparing a comprehensive budget proposing how funds shall be spent, and actually handling the use of funds. The Constitution Act, 1867 states:

It shall not be lawful for the House of Commons to adopt or pass any Vote, Resolution, Address, or Bill for the Appropriation of any Part of the Public Revenue, or of any Tax or Impost, to any Purpose that has not been first recommended to that House by Message of the Governor General in the Session in which such Vote, Resolution, Address, or Bill is proposed.55

The language of the Constitution is echoed in the Standing Orders of the House of Commons.56

For the first 100 years following Confederation, any bill or clause appropriating money had to be preceded by a House resolution, the wording of which defined precisely the amount and purpose of any appropriations sought. The resolution was moved by a Minister of the Crown and was recommended by the Governor General.57 Every appropriating clause of the subsequent bill had to conform to the provisions outlined in the resolution, and no Member could move amendments to the legislation that would have the effect of increasing the amount or altering the purposes which the resolution had authorized.58 To alter an appropriating clause, the government had first to obtain a new resolution from the House, again recommended by the Governor General, embodying the change.

Because the debate on the financial resolution was often repeated at the second reading stage of the bill, the House eliminated the resolution stage in 1968.59 The Crown’s recommendation would now be conveyed to the House as a printed notice which would appear on the Notice Paper and again in the Journals when the bill was introduced, and be printed in or appended to the bill.60 The rule change did not alter the constitutional requirement for a royal recommendation, only the procedure to be followed.

Detailed recommendations were printed until 1976, when the government began using the current formula, which is as follows:

His/Her Excellency the Governor General recommends to the House of Commons the appropriation of public revenue under the circumstances, in the manner and for the purposes set out in a measure entitled (long title of the bill).61

In 1994, the Standing Orders were again amended to remove the requirement that a royal recommendation had to be provided to the House before a bill could be introduced.62 The royal recommendation can now be provided after the bill has been introduced in the House, as long as it is done before the bill is read a third time and passed. However, the government has maintained the practice of providing the royal recommendation to its bills at the moment they are put on notice for introduction in the House.63 The royal recommendation accompanying a bill must appear on the Notice Paper for a 48-hour period, printed in or appended to the bill and recorded in the Journals before the question can be put at third reading of a bill.

As a royal recommendation may be obtained only by a Minister of the Crown, and because Ministers do not usually sit on committees, any amendment calling for additional public spending may be proposed and considered only at report stage. If necessary, the Minister puts the royal recommendation accompanying each motion in amendment at the report stage on the Notice Paper.64 The notice period is 24 hours when consideration of the report stage of the bill takes place after second reading, or 48 hours when it takes place at second reading.65 If a royal recommendation is placed on notice, it is entered in the Journals for the sitting during which the motion in amendment at the report stage referred to in the royal recommendation is moved and seconded.66 It also appears in the version of the bill adopted by the House of Commons at third reading.

In general, there are two types of bills which confer parliamentary authority to spend and therefore require a royal recommendation:67

- appropriation acts, or supply bills, which authorize charges against the Consolidated Revenue Fund up to the amounts approved in the estimates; and

- bills which authorize new charges for purposes not anticipated in the estimates.68 The charge imposed by the legislation must be “new and distinct”; in other words, not covered elsewhere by some more general authorization.69

An appropriation accompanied by a royal recommendation, though it can be reduced, can neither be increased nor redirected without a new recommendation.70 Because financial legislation must originate in the House of Commons, bills that require a royal recommendation may not be introduced in the Senate.71

A royal recommendation not only fixes the allowable charge, but also its objects, purposes, conditions and qualifications. For this reason, a royal recommendation is required not only in the case where money is being appropriated, but also in the case where the authorization to spend for a specific purpose is significantly altered.72 Without a royal recommendation, a bill that either increases the amount of an appropriation or extends its objects, purposes, conditions and qualifications is inadmissible on the grounds that it infringes on the Crown’s financial initiative.73 However, a royal recommendation is not required for a bill whose effect is to reduce taxes otherwise payable.74

Since the mid-1990s, and especially since 2005, there have been many Speakers’ rulings on cases relating to the royal recommendation. Almost invariably, these precedents have involved public bills sponsored by private Members on which points of order have been raised and in which the Chair’s ruling has considered the unique and specific provisions of each particular bill.75

Royal Recommendation and Public Bills Sponsored by Private Members

In the past, when a public bill sponsored by a private Member infringed on the financial initiative of the Crown, the Speaker did not allow it to go forward.76 However, ever since Standing Order 79 was changed in 1994, private Members’ bills involving the spending of public money have been allowed to proceed through the legislative process on the assumption that a royal recommendation will be submitted by a Minister of the Crown before the bill is to be read a third time and passed.77 If a royal recommendation is not produced by the time the House is ready to decide on the motion for third reading of the bill, the Speaker must stop the proceedings and rule the bill out of order.78

Under Standing Order 79(2), the royal recommendation accompanying a bill must be published in the Notice Paper, printed in or annexed to the bill and recorded in the Journals. Since 48-hours’ notice is required and only two one-hour periods are allocated to the report stage and third reading for a public bill sponsored by a private Member, the royal recommendation must be placed on notice at least 48-hours before the second one-hour period for the consideration of the measure in question. Whether debate concludes during the first hour, or the second hour, the Speaker will refuse to put the question to a vote at the conclusion of the debate and will rule the bill out of order in the absence of a royal recommendation. In the event that a royal recommendation is placed on notice, it will appear in the Journals for the sitting during which the order is called for consideration of the bill to which the recommendation applies. It will also appear in the version of the bill as adopted by the House of Commons at third reading.

In March 2003, the House adopted a comprehensive reform of the provisions of the Standing Orders governing the consideration of private Members’ business.79 These changes led the House to pay greater attention to the royal recommendation. As a result of the reforms adopted in 2003, the number of private Member’s bills that can be submitted to a vote has increased, and more of these bills can now reach third reading.80 Moreover, since those Members entitled to do so should, in principle, be able to have a measure debated in the House of Commons at least once each Parliament, the Speaker wants to give them every possible opportunity to correct any procedural faults their bills might have. Therefore, a number of novel practices have been instituted.

When it appears almost certain that a private Member’s bill will require a royal recommendation, a team of legislative counsel and procedural clerks promptly informs the sponsor so that the latter can make any necessary changes. At the same time, after reviewing all the bills on the Order of Precedence at the beginning of a Parliament, the Speaker communicates to the House a list of those which at first glance could appear to infringe on the financial prerogative of the Crown. The Speaker then invites the Members to explain why, in their view, each of these bills require a royal recommendation or not.81 The Speaker will then hear these points of order at the appropriate time and will normally make a ruling before the second hour of debate begins.82 If necessary, the Speaker will make a definitive ruling at a later point in the legislative process.83 This review also takes place at the beginning of a new session,84 and when the Order of Precedence for Private Members’ Business is replenished.85

The Speaker has the duty and responsibility to ensure that the Standing Orders pertaining to the royal recommendation, as well as the constitutional requirements, are upheld. There is no provision under the rules of financial procedure that would permit the Speaker to leave it up to the House to decide or to allow the House to do so by unanimous consent. These imponderables apply regardless of the composition of the House.86

The Commons’ Claim to Predominance in Financial Matters

The Constitution and the Standing Orders of the House of Commons require that bills which appropriate (impose a charge on the public revenue) or levy any tax or duty (impose a charge upon the people) must first be introduced and passed in the House of Commons.87 The Speaker has ruled that a Senate bill which appropriated public money could not be read the first time in the House and directed that the notice for the first reading of the bill be removed from the Order Paper.88 The Speaker has also ruled that a Senate bill which had been read a first time in the House was in fact imposing a tax and should have originated in the Commons; the proceedings on the bill were declared null and void and the bill was ordered withdrawn from the Order Paper.89

Financial legislation is, in the opinion of the House, not alterable by the Senate.90 Since Confederation, the Senate has occasionally asserted the right to amend money bills.91 Most of the disagreements between the two Chambers arise over the extent of the Senate’s authority to amend financial legislation. On the one hand, it has been argued that the Senate is restricted to passing or rejecting such bills.92 Others maintain that the Senate has full powers to amend, provided that it does not increase appropriations or the amount of taxation.93 The issue is whether a money bill is one which includes any financial provisions or whether its purpose must be primarily or solely financial and, consequently, whether any restrictions on the Senate’s power to amend should extend to the whole bill or simply to its financial aspects. A further question is whether or not the Senate can propose amendments to bills amending existing financial legislation.94 In some instances, the House of Commons has rejected the Senate’s amendments and claimed its financial privilege.95 On other occasions, however, the House has waived its privileges and accepted the Senate amendments.96 Where the Commons choose to accept a Senate amendment (to a bill appropriating funds or imposing a tax), they usually waive their financial prerogative, while insisting that their decision in this instance does not constitute a precedent.97 However, the House, on occasion, has accepted or rejected amendments with no reference made to its privileges whatsoever.98 On at least two occasions, the Speaker has refused to lay aside Senate amendments to financial legislation, maintaining that it is the responsibility of the Commons, not the Chair, to invoke or waive the privileges claimed by the House.99 Although the Chair has acknowledged its responsibility for directing the House’s attention to any Senate bill or amendment which breaches its privileges,100 the Speaker does not rule on the right of the Senate to amend financial legislation on the grounds that this is a constitutional issue.101 Senate bills, on the other hand, have been laid aside on the grounds that they contravened the constitutional principles that financial bills originate in the Commons and are introduced at the initiative of the Crown.102

The House will allow the Senate to include or alter pecuniary penalties in bills, where such penalties seek only to punish or prevent crimes or offences and do not have the effect of incurring a public expenditure or imposing a tax on the people.103